Modern mythmaking tells us that the most successful business ventures start in workaday, somewhat solitary venues — dorm rooms, garages, and the like — where, through grit and genius, a “lone founder” can turn a promising idea into a runaway commercial success. Yet history (and, frankly, the realities of community and capitalism) suggest that, in truth, most companies’ geneses are far more social than our “lone founder” myth implies.

Accelerant, which IPOs on the New York Stock Exchange today at a market value around $4.7 billion, got its start at a watering hole. In December 2018 in Stockholm, insurance veterans Jeff Radke and Chris Lee-Smith griped over dinner and drinks about the state of the market for smaller players. More data than ever existed regarding specific and systemic risk, but the platforms and services that could ingest that data and make it useful for specialist insurers were antiquated and inadequate.

“We couldn’t accept that, in this digital era, less than 10% of data collected for underwriting actually made it through the system,” Radke recalled in a February interview with Fintech Nexus. “We grabbed a napkin and started sketching out a vision for how the industry could work more efficiently and fairly.”

Its founding myth partially echoes that of insurance giant Lloyd’s of London. The Lloyd’s Coffee House opened in 1686 on Tower Street in London, offering a generous flow of java as well as a steady stream of information about shipping and the seas thanks to its mercantile clientele. This bustling, decidedly interpersonal forum became the go-to destination for maritime insurance, eventually turning into the insurance and reinsurance market that remains shorthand of sorts for insurance itself. A subset of Lloyd’s patrons, separating themselves from the network’s speculative undertones, formally established an insurance society and marketplace with a commonly agreed-upon set of commercial and underwriting practices, culminating in special Parliamentary recognition of Lloyd’s of London by 1871.

But even in this later iteration, the flow of information (coffee-house style) was key to making the insurance trade a true marketplace. According to Dr. Hannah Farber, associate professor of history at Columbia University and author of Underwriters of the United States: How Insurance Shaped the American Founding, “expertise is one of the things that distinguishes insurance from gambling.”

Without empirical rules determining whether a risk is reasonable or not, deep knowledge of a field, up-to-date information, and clear regulation are core to steering practitioners away from “rolling the dice” and herding them closer to “actuarial science.”

In this vein — and in fits and starts — the insurance industry has occasionally erected institutional scaffolding that rewards expertise over other qualities. The subfield of managing general agents (MGAs), for example, is part of that effort; MGAs often cater to geographies or niche industries that insurance carriers and brokers do not serve. Especially after the National Association of Insurance Commissioners (NAIC) revamped regulation around MGA practices in 2002, this agent type has proliferated: Its growth rate has outpaced that of the larger property and casualty space, driven by talent incentives, technological developments, and challenger advantages over larger carriers. But the 1100-some MGAs in the United States have lacked a network of their own, often dependent on the whims of larger players to carry out their business. In other words, MGAs have needed a coffee shop.

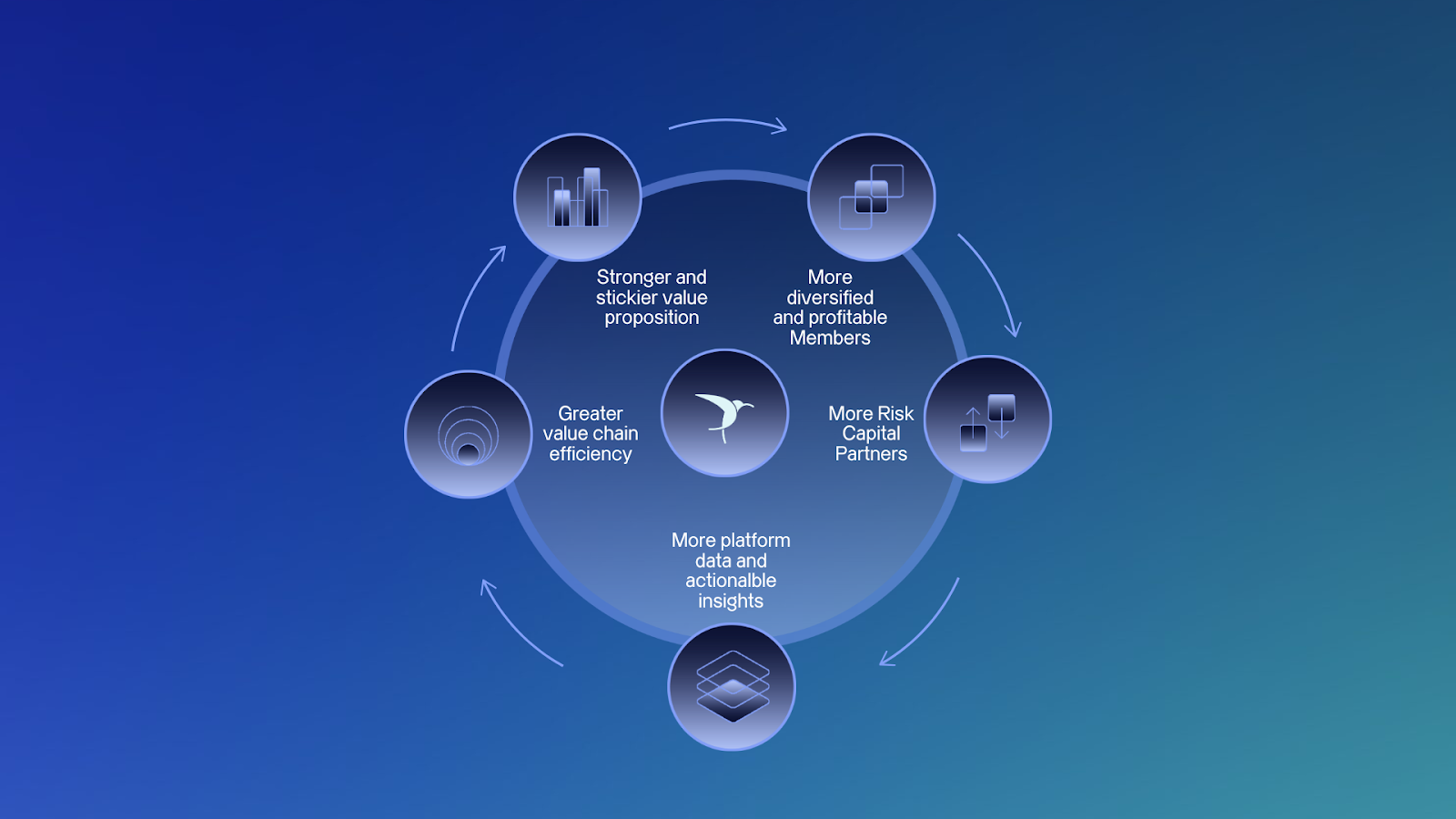

Like Lloyd’s, Accelerant’s development has required several iterations. Over time, it’s built out sidecars and subsidiaries to generate a technologized forum for data-driven specialized insurance — wherein capital providers such as insurance and reinsurance companies can fund MGA activity and MGAs can enjoy uninterrupted access to capacity — while also bolstering the supply and demand of capital and risk within its exchange.

Over the past seven years, Accelerant has converted more than 200 MGAs into platform participants, who, after joining, have grown 43% per year on average. Nearly 100 capital providers have joined Accelerant as well, while Accelerant itself has ballooned into an enterprise with $3.5 billion in premium volume on the platform and with some 400 employees.

Accelerant’s public debut makes it one of the relatively few insurtechs to have entered the public market in recent years. This uncharted territory — laden with compliance and reporting obligations, new investment imperatives, as well as the public-market history of insurtechs of yore — represents a new challenge. However, if launched and scaled successfully, Accelerant may help consolidate MGA practices so that the subsector functions less like a pack of “lone founders” and more like a marketplace.

ASSURANCES FOR INSURANCE

It’s no longer commonly assumed that first movers can rely on network effects alone to solidify their hold on a nascent market.

“The reason is that chasing early growth before a marketplace has proved its value to both buyers and sellers leaves the business vulnerable to competition from later entrants,” business school professor Andrei Hagiu and Greylock partner Simon Rothman explained in 2016. “If either side’s users do not derive significant value on a consistent basis, they will readily jump ship.”

The authors argue that one way to keep a marketplace network strong is to “provide insurance to one or both parties in a transaction.” That doesn’t necessarily mean insurance in the literal, actuarial sense. Accelerant’s brand-defining version of this is its five-year capacity guarantee, which addresses an existential pain point for MGAs. Over 70% of MGAs agree that it is hard to find capacity to support new programs, which holds back expansion and forces them to dedicate time and resources to ancillary fundraising tasks.

In an interview with the Insurance Nerds podcast, Radke said it’s “fun to back someone older” in the MGA space who is used to “the drudgery of running around London or running around Bermuda with your hat in your hand trying to secure capacity for next year.”

“If that all goes away, it’s like they’re 25 again,” he joked.

But this isn’t an altruistic (or anti-aging) arrangement. In exchange, the MGAs hand over all their data to Accelerant, which in turn tries to help the MGA make sense of it. Whereas capacity guarantees are the kick-start, Accelerant thinks data is the grease for its flywheel over the long run.

This aligns with contemporary network-effects theory as described by Eddie Yoon, a Hawaii-based strategic growth advisor. In a co-authored Harvard Business Review piece from 2019 (the last one mentioned in this article, we promise), Yoon argues that the difference between a “first mover” and a “category creator” (many of which become shorthand for their subsector) is a “high-functioning flywheel”:

the combination of 1) a radical product/service innovation, combined with 2) a breakthrough business model innovation, and finally greased by 3) a breakthrough big data about future category demand.

In an email interview with Fintech Nexus, Yoon updated his article’s takeaways for 2025, centering the potential effects of automation on first movers’ moats. Proposing that cost advantages, performance advantages, and customer-experience advantages are three primary moats for businesses, Yoon said companies that “rely on cost and performance as their moat will find AI, automation, and other technologies to drain their moats and make them fleeting advantages.”

However, Radke seemed to disagree with how Yoon framed the relationship between automation and competitive advantages; Radke depicted Accelerant’s data as a robust moat — in his words, “the broadest specialty insurance data set that’s usable in the market.” The company holds more than 79 million rows of proprietary risk data, 21,000 unique risk attributes, and is ingesting around 8.9M new rows per month, per its S-1 filing with the Securities and Exchange Commission (SEC). Accelerant’s net promoter score (NPS) of 89 suggests customers are motivated to stick around too, further driven by its low-50s loss ratios.

Radke highlighted the need for incentives to align across its Members and the partners paying them.

“Our model is we get paid a fee to source, manage, and monitor a portfolio of specialty insurance on behalf of risk capital,” he said. “If our performance went from market-leading loss ratios to market-trailing loss ratios, it’s pretty simple that people wouldn’t pay us to source, manage, or monitor that portfolio.”

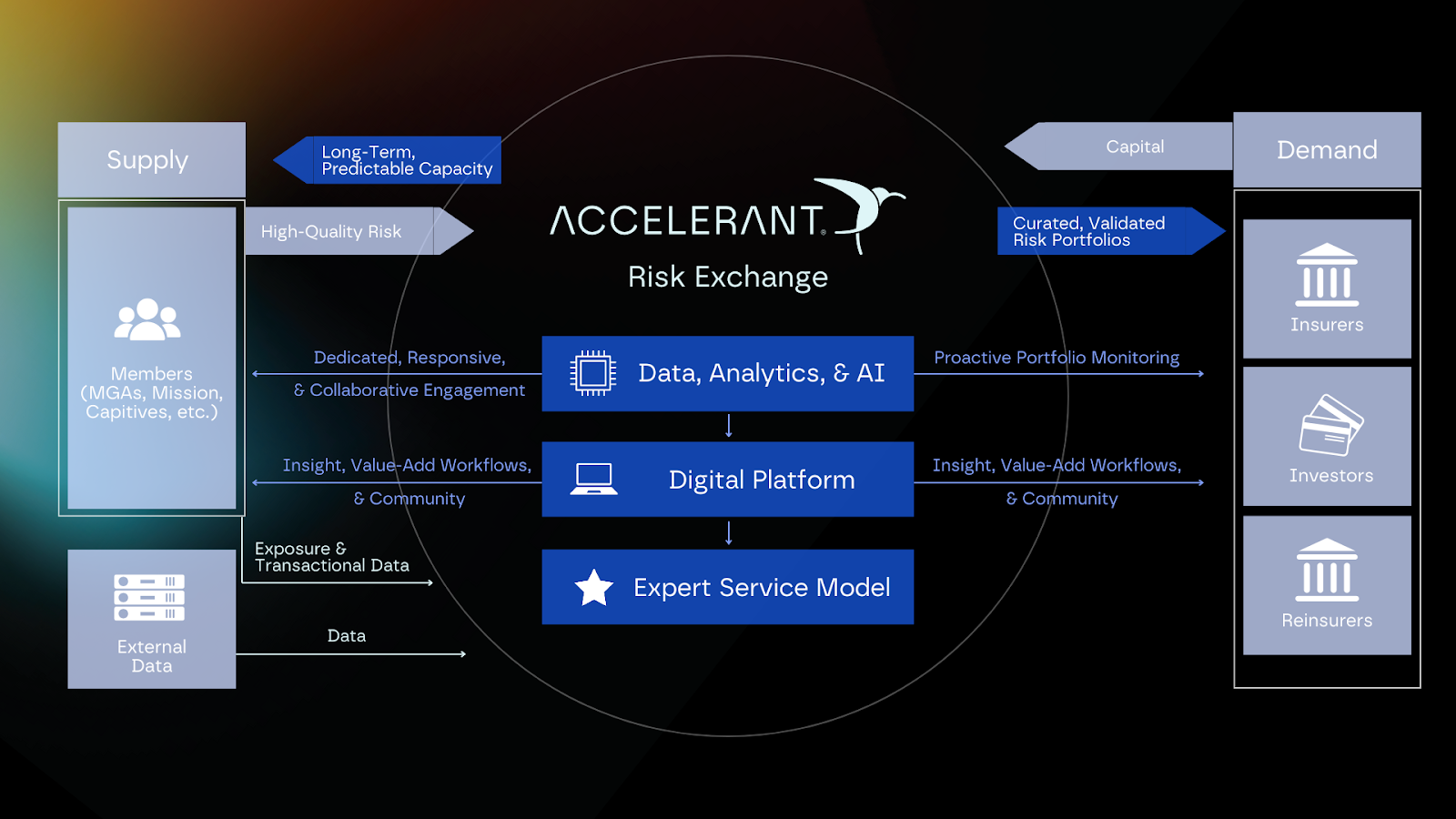

In part, this divergence in thinking may be because, for Accelerant, data used in automation is a performance driver as well as a customer-experience driver. According to documents viewed by Fintech Nexus, the company believes “There should be a Bloomberg of specialty insurance — the default access point and data source for all specialty risk.” With MGA customers (or “Members” in their parlance) integrating all data into the platform, Accelerant can build a Bloomberg Terminal of sorts for the risk economy, while also feeding those inputs into AI models that can automate underwriting and risk-evaluation tasks.

SPINOFFS, SUBSIDIARIES, and SIDECARS

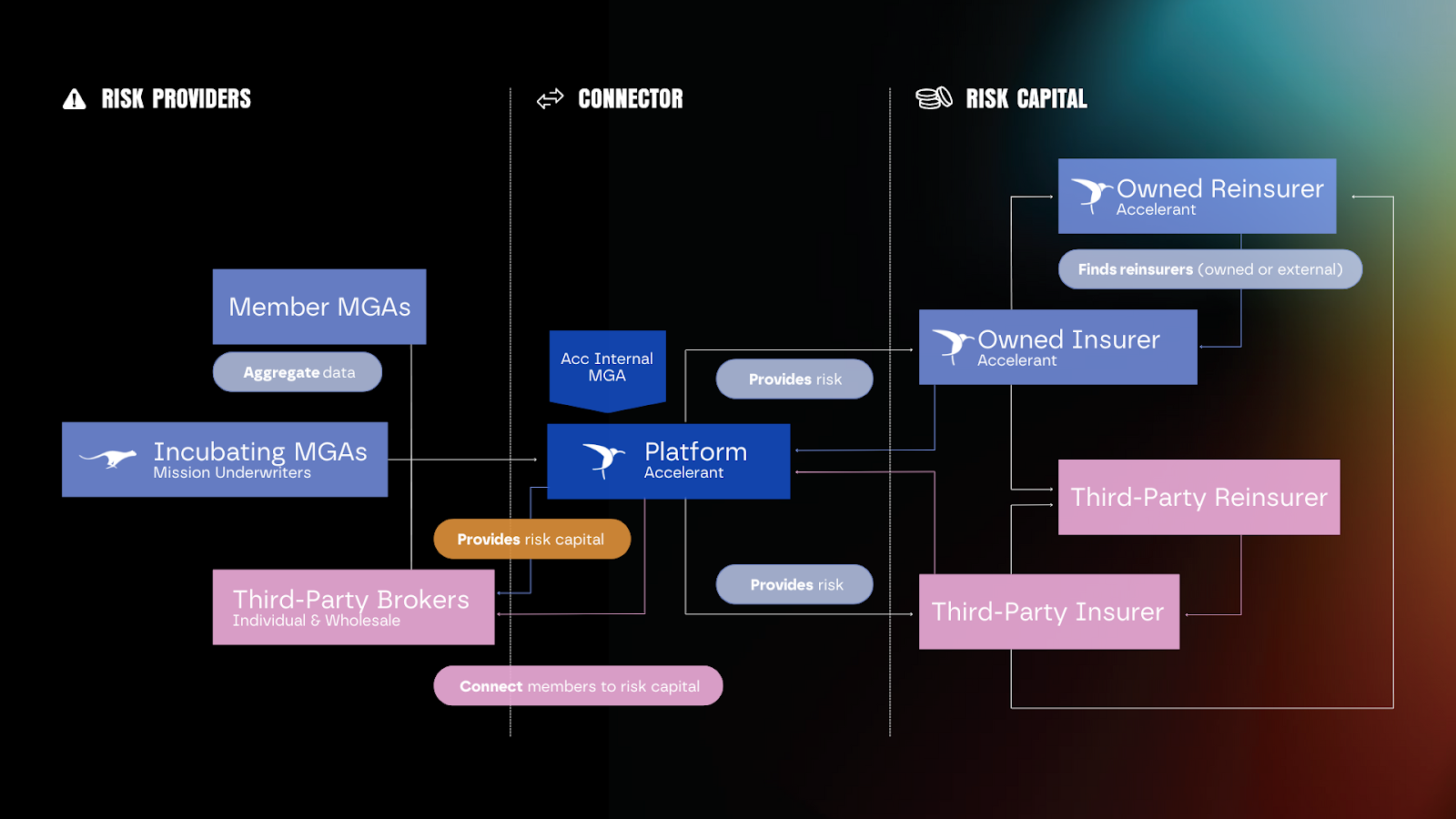

Core to Accelerant’s process-efficiency ambitions is its self-identified function as a utility of sorts. Whereas different players previously possessed their own proprietary infrastructure — databases, capital management systems, and other core tools — Accelerant can serve as those rails for an entire subsector. “You get so much efficiency out of putting that on one modern platform,” Radke said. “We figure the frictional expenses are about half on the Accelerant platform compared to what the average industry spends.”

The utility has grown more complicated over the years by tackling different pain points within specialized insurance, making it something of a corporate hydra. It includes Mission Underwriters, which incubates MGAs by offering wraparound operational services that let startup specialty underwriters focus on their primary job (underwriting).

These factions (proprietary and third-party) all feed into and constitute part of Accelerant’s Risk Exchange. In Accelerant’s diachronic view, owning what it dubs the “means of connection” and replatforming a value chain can transform into a larger ecosystem with far greater potential.

FUNDING AND FUNDAMENTALS

Sourcing, refining, deploying, underwriting, and sustaining a data flow that transmutes workaday actuarial inputs into a tripartite flywheel and sticky platform is no cheap undertaking. Prior to its public debut, Accelerant raised hundreds of millions in private equity funding. In its most recent public raise from June 2023, Barings injected $150 million into the platform at a $2.3 billion valuation. Eldridge Industries led its 2022 fundraise ($190 million+), which also included MS&AD Ventures, Marshall Wace, Deer Park Road, and Altamont Capital Partners, which was the founding investor in Accelerant and remains its largest shareholder.

By contrast, Ledger Investing, arguably Accelerant’s most direct competitor, has raised just over $90 million in venture funding, including a 2022 Series B of $75 million. Ledger also secured a $100 million reinsurance sidecar through a (nameless) global reinsurer in September 2024 and syndicated a $250 million secondary transaction with three institutional investors in August 2023. It spun out of startup incubator Y Combinator in 2017 — a full year before Accelerant’s napkin-borne birth, perhaps laying claim to the first-mover crown.

In Radke’s view, Altamont was “particularly good at investing in insurance” and “particularly good at being partners to management,” which was partially why Accelerant landed with Altamont as a majority investor. But why private equity?

“When we started the business, the business proposition didn’t feel to us, nor to any of the VCs, like a VC opportunity,” Radke told Fintech Nexus. “It was relatively capital-significant right from the beginning. And it wasn’t the kind of thing where you were going to put in a tiny amount of capital, do four seed rounds, and off you go.

“We’re setting out to do something that hasn’t been done for quite some time, since Lloyd’s 354 years ago. We knew this was going to take a fair amount of money and a fair amount of time, and neither of those things tend to sort of match very well with the VC side. So I suspect VCs wouldn’t have been interested in an Accelerant offering,” Radke continued. “It was much more of a PE fit in terms of scale and time horizon.”

THE RISKS OF A RISK EXCHANGE

Public-market success isn’t guaranteed, however. Investors may hope AI-inflected insurtech brings on better days when they look at how previous insurtechs have fared, even if their business models are different. Root (NSDQ: ROOT), Hippo (NYSE: HIPO), and MetroMile all floundered post-IPO; Lemonade (NYSE: LMND) went public in July 2020 at $29 a share, and now hovers around $35. (Granted, some used special purpose acquisition companies, or SPACs, to enter the stock market.)

And less-than-savory business practices have previously plagued the subsector. Vesttoo, an Israel-based insurtech, allegedly used fraudulent letters of credit (LOCs) to collateralize insurance transactions. Court filings suggest Vesttoo blames co-founder and former CEO Yaniv Bertele, co-founder and former chief financial engineer Alon Lifshitz, as well as three other employees for the fraudulent activity.

Following the outbreak of the scandal, Accelerant Specialty Insurance Co. reported that a $13.5 million LOC was “invalid,” forcing the company to establish a $19.2 million provision to account for the loss. That paled in comparison to other victims. Subsidiaries of Clear Blue Insurance Group LLC, for instance, held over $500 million in LOCs from China Construction Bank Corp, the bank falsely attributed to Vesttoo’s LOCs. Even as insurers readjusted and recovered, the systemic and reputational implications may be more profound.

MGA-focused market research from Conning suggests that over 80% of MGAs do not see the Vesttoo scandal as having affected their business, but it’s difficult to extrapolate from finite transactions to gauge public-market sentiment. These same investors may see the forms of compliance and reporting requisite of a publicly traded company as an added benefit — or they may see it as burdensome overhead that affects Accelerant’s unit economics.

More recently, Accelerant has encountered some of the marginal risks that can arise when expanding through partnerships. In France, a kerfuffle emerged when it was revealed that Assurances Pilliot, a broker specializing in motor insurance, had issued policies it claimed were backed by Accelerant Insurance Europe (AIE). However, AIE had not authorized these policies, nor did it have the regulatory authority to issue that kind of insurance coverage. A regional commercial court in France ordered Pilliot to immediately cease the practice, notify clients of the invalid status of their policies, and provide Accelerant with a list of affected clients and vehicles — totaling around 75,000 in France. Though the court attributed the snafu to the broker, the episode highlighted the reputational and operational risks Accelerant faces when partners fall short of compliance expectations.

Accelerant’s S-1 filing outlines a litany of risks associated with its line of business (as businesses entering the public market are expected to do). These include potential regulatory changes to how MGAs are treated, rising oversight costs, increased loss ratios, systemic risks like climate change, the departure of risk exchange members for a competitor or other reasons, rejections or slow approvals from reinsurers, defaults at financial institutions where Accelerant holds cash, and many other variables.

Some other risk factors are named less explicitly in the filing. Accelerant’s deployment of artificial intelligence, for instance, reflects larger public-market enthusiasm for AI while also representing a potential liability. In an interview with Bloomberg, Radke claimed that the injection of AI and machine learning (ML) into the risk exchange had led to a 20% improvement in margins. AI is playing a growing role in determining where MGAs expand their portfolio and adjust policies, Radke said.

AI-focused companies may largely enjoy a laissez-faire regulatory environment during the current presidential administration, but that is not guaranteed on a state-by-state basis or over the long run as public concern around data and privacy continues to mount. Accelerant may have to furnish interpretable and explainable models, or fundamentally alter how AI and ML are deployed on its platform, or accept that it might eventually be illegal to sell the data it collects to third-party entities. In the long run, Accelerant’s members may confront the supposed negative correlation between generative-AI use and critical-thinking capacity — which may eventually encourage MGAs to conduct business through more analog means or through tweaked deployments of AI. The insurance industry has ostensibly outgrown its gambling-ish origins; relinquishing control over key business decisions to often inscrutable technological tools seems like a step back. Other potential societal effects may elicit regulatory intervention. In other insurance markets, the whittling of risk portfolios has led to more businesses and consumers remaining uninsured; while that sometimes encourages these entities to adopt less risky practices or move to safer markets, it can also create a “haves” and “have nots” bifurcation with deleterious social outcomes (higher rates of bankruptcy, poverty, etc.).

The insurance sector writ large also has a long, demonstrated history of re-entrenching racial discrimination. From Lloyd’s underwriting the transatlantic slave trade to the practice of redlining, it’s hard to claim that the blind pursuit of risk quantification and mitigation has furnished consistently positive social outcomes. Partially in response to these realities, many jurisdictions impose anti-discrimination statutes that govern the kinds of information that insurers can collect about potential customers, and influence how insurers serve markets in terms of pricing distribution and geographic spread.

“Because we write commercial business, we escape a lot of personal problems, but not all,” Radke said. “When we behave in a way that makes us regulatory and legally compliant, I’m awfully comfortable that we’re not doing something that I’m uncomfortable with.”

At the same time, Radke conceded that the complexity of Accelerant’s business, which involves interacting with more than 60 regulatory bodies, is a variable that “could go wrong.” Regulators down the road may see “utility”-like aspirations as warranting antitrust scrutiny, too.

As Farber, the historian of insurance, put it in her interview with Fintech Nexus: “There’s no such thing as a giant international financial business that’s not political … It can still be very hard to see.”

And then there’s Lloyd’s. Having sourced $7.5B of premium from US MGAs in 2023, Lloyd’s hovers over the MGA landscape and continues to shape it in its image. Can Accelerant convincingly square up against the coffee house-brewed behemoth? To be sure, market leaders no longer congregate at literal coffee shops to gauge winners and losers — there’s a stock market for that — but Accelerant’s capacity to live up to its aspirations may well determine whether MGAs can build a marketplace of their own, and scale from there.

What’s next? Radke takes a long view to frame what insurance-technology platforms can and should accomplish. He sees insurtech history as possessing three phases to date. The first phase, Insurtech 1.0, was about customer acquisition. The second phase, Insurtech 2.0, included mass-market products, like personal lines, and pushed for faster and cheaper underwriting processes.

“Version three is where I consider Accelerant to be,” Radke said. “There’s a focus on how you are going to use data and analytics to make smart decisions and technology to make efficient processes.”